A geometric gradient series grows (or shrinks) by a constant percentage each period. If the first-period cash flow is at time 1, then the cash flow in period is

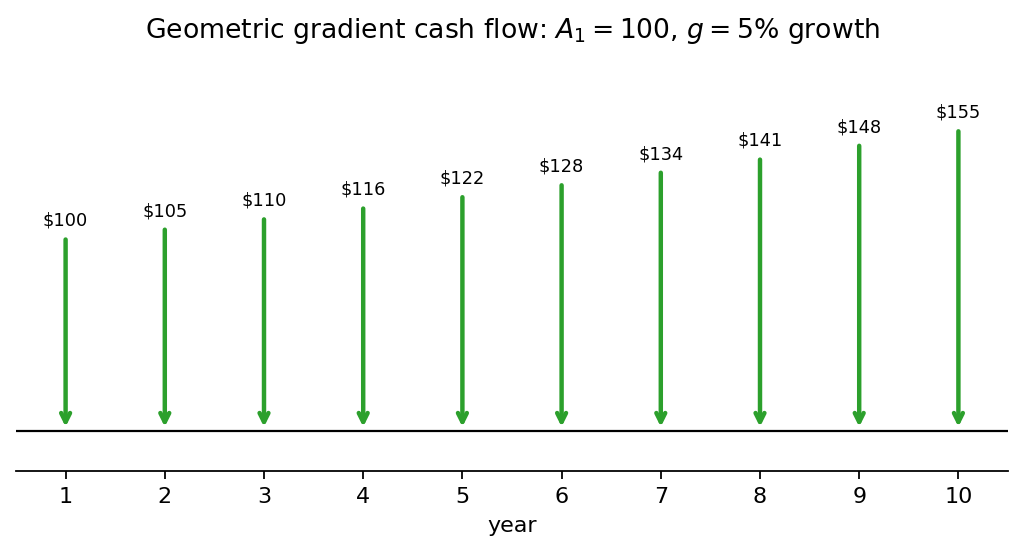

Geometric gradient cash flow: , growth %/yr. Each year’s payment is .

Geometric gradient cash flow: , growth %/yr. Each year’s payment is .

The total present worth at rate over periods has a closed form. Let (the adjusted interest rate left after stripping growth). Then

When exactly (growth matches interest), the discount and growth exactly cancel and the present worth is .

Most of the time you evaluate these in a spreadsheet rather than by factor lookup. Type out the cash flow column , discount each one with , then sum. Mechanical, and you don’t have to worry about which factor applies.

Geometric gradients fit cash flows that escalate with Inflation (prices and wages usually grow by a percentage each year, not a constant dollar amount), revenues in a growing market, or costs in a learning-curve industry, where each doubling cuts cost by a constant fraction (a negative geometric gradient on cost).

Special case: if each period’s cash flow scales with general inflation, then the real present worth, using the Real interest rate instead of nominal , strips out the growth factor and the geometric gradient becomes a pure annuity in real terms. This is why inflation analyses often switch between real and actual dollars: a geometric gradient in actual dollars can be a uniform annuity in real dollars.

For the linear cousin (constant additive increase per period), see Arithmetic gradient series.